Tax instalments are scheduled payments to the Canada Revenue Agency (CRA) that cover a portion of your annual tax bill as you earn income. Instead of a lump‐sum yearly payment, you make smaller advance payments, similar to the way employers withhold tax from paycheques. This guide breaks down when taxes must be paid by instalments, as well as the key due dates and calculation methods involved.

Who Needs to Pay Instalments?

Whether you run a corporation, a sole proprietorship, or are registered for GST/HST, the CRA sets thresholds that trigger instalment requirements.

Corporate Tax Instalments – Most Canadian corporations must pay tax by instalments. Under the Income Tax Act, if a corporation’s total tax owed exceeds $3,000 in a tax year, it generally must remit instalments in the following year. Newly‑incorporated companies may get a first‑year break, meaning they don’t have to make instalments until their second fiscal year.

Personal Tax Instalments – Self‑employed individuals and other taxpayers may also need to pay by instalments. You generally must pay instalments if your net tax owing exceeds $3,000 in the current or any of the past two years (the Quebec threshold is $1,800).

GST/HST Instalments – Any business (incorporated or not) that is a GST/HST registrant may also need to make instalment payments for sales tax. Annual filers whose net GST/HST owing was $3,000 or more in the previous year must pay quarterly instalments in the current year.

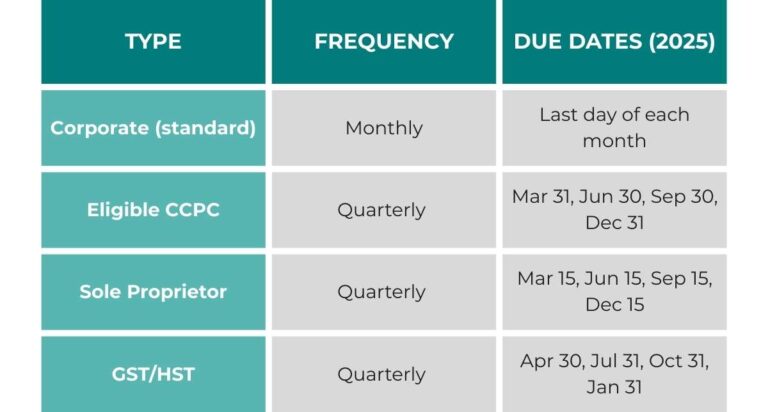

When Are Tax Instalments Due?

Most corporations default to monthly instalments, while eligible small Canadian-controlled private corporations (CCPCs) can opt for quarterly payments. Self-employed individuals and GST/HST registrants generally also follow a quarterly instalment schedule.

Corporate Tax Instalments – By default, corporate instalments are due monthly. The first payment must be made one month less a day after the start of your fiscal year, then monthly thereafter. However, eligible CCPCs may opt for just four quarterly instalments instead of twelve. To qualify for quarterly instalments, a CCPC must have a perfect compliance history, with taxable income of $500,000 or less and taxable capital employed in Canada for the tax year of $10 million or less.

Personal Tax Instalments – Installments for individuals are due on fixed dates: March 15, June 15, September 15, and December 15 (except farmers/fishers, who pay once on December 31).

GST/HST Installments – GST/HST instalments are due one month after each fiscal quarter ends. For example, a business with a December 31 year-end would have instalments due April 30, July 31, October 31, and January 31.

For a summary of the various tax instalments and their due dates, see the table below. Note: If a due date falls on a weekend or holiday, the next business day applies.

How to Calculate Your Tax Installments

The CRA offers three options for calculating instalment amounts. Taxpayers can use the amount outlined by the CRA in their instalment reminders, use the previous year’s tax liability, or estimate current profits. Businesses should select the option that best matches their cash flow and income volatility:

No-Calculation Option – Use the CRA’s suggested amounts from your instalment reminder. Best for stability and avoiding interest.

Prior-Year Option – Divide last year’s total tax owing by the number of payments (12 monthly or four quarterly). Ideal when income is consistent year-over-year.

Current-Year Option – Estimate your current year’s tax and split it across instalments. A good choice for businesses expecting lower income, just be aware that underpayment can result in interest.

For corporations, using the CRA’s suggested amounts (from their reminders) is generally safest, as you won’t incur interest even if your actual tax bill changes. Sole proprietors, on the other hand, generally use the prior‑year safe-harbour calculation for simplicity.

Final Thoughts

By understanding CRA installment rules, aligning payment schedules with your cash flow, and picking the right calculation method, you’ll keep your business compliant, avoid unnecessary interest, and maintain peace of mind year-round. Be sure to take advantage of the CRA’s tools and worksheets, and if you have questions or need tailored guidance, reach out to your trusted financial advisor.

This article was written by the NVS Professional Corporation team, your knowledgeable Barrie and Markham accountants. The content is intended as a general guide for informational purposes only. For specialist advice tailored to your specific situation, please reach out to our expert team.